Oregon can't catch a break: Preliminary 2027 unsubsidized ACA rate filings: Indy mkt up 17%, sm. group mkt up 16%

Fri, 06/05/2026 - 8:54am

The past couple of weeks have been pretty brutal for the Oregon health insurance market.

On May 21st, Providence Health Plan announced that they were shutting down pretty much their entire insurance division across Oregon (which also impacts some people in Washington and California):

Providence Health & Services plans to exit most of its Oregon health insurance business next year, citing rising costs, tougher regulation and intensifying competition from national insurers — a move that will force hundreds of thousands of Oregonians to find new coverage.

...Providence Health Plan, based in Portland, is Oregon’s third-largest health insurer, covering more than 421,000 Oregonians. It also covers over 13,000 members in Washington and 4,800 in California.

Providence had around 40,000 ACA indy market enrollees as of a year ago...I don't know exactly how many they have today, but assuming the same ~15% y/y drop they had statewide, that would be perhaps ~34,000 now.

Then, a week later, PacificSource announced that they're dropping out of the Oregon individual market next year as well (although they aren't shutting down all insurance divisions). That should mean another ~18,000 or so current enrollees who will have to shop around next year.

PacificSource, the Oregon-based health insurer, is pulling out of Montana and leaving the individual market while cutting staff.

The number of people who could be affected in this new round of layoffs is unclear, but this week the not-for-profit slashed four high-level executives. Based on the types of plans affected by the insurer's latest restructuring some dozens more pink slips are expected to go out starting next week.

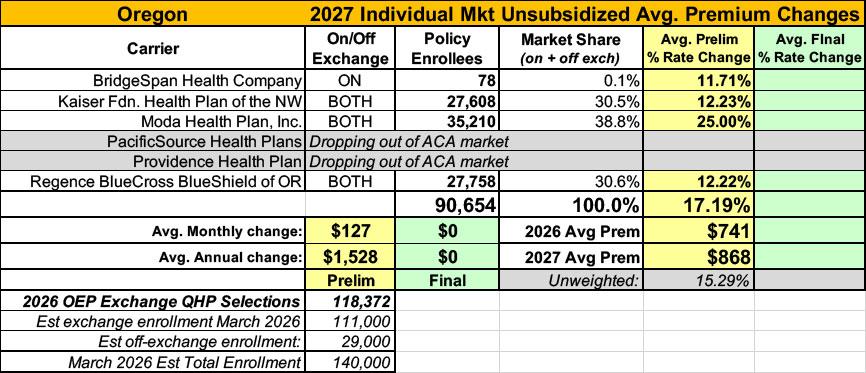

By my best estimates, Oregon's total individual market (which includes some off-exchange enrollees) should be roughly 140,000 people today, around 37% of whom will have to find new coverage via one of the four remaining carriers in the state...which brings us to today's update (shout-out to Nick Budnick of The Lund Report for the heads up that Oregon's filings are available:

BridgeSpan Health Company:

This filing proposes an average annual rate change of 11.7% at January 1, 2027, for the Individual line of business, as shown in “Exhibit 1: Development of Rate Change.” The 2027 projected average premium is $951.33 per member per month (PMPM).

The average annual rate change is calculated based on Individual enrollment data as of March 2026 and includes the mapped rate impact for membership enrolled in plans terminating in 2027. A summary of the rate changes by plan is shown in “Exhibit D1: 2027 Average Change in Plan Base Rates.”

The estimated distribution of member-level rate changes due to changes in base rates, plan relativities, rating factors, and plan mappings is as follows:

Rate Change / Distribution

- 8.0% to 11.0% / 34.6%

- 11.0% to 14.0% / 57.7%

- 14.0% to 17.0% / 7.7%

The benefit plans impacted by the rate change request are shown in “Exhibit 6: Plan Relativities.”

This filing assumes Cost Sharing Reduction (CSR) payments will not be paid in 2027. If changes are made to the premium subsidies, risk adjustment, or reinsurance, the proposed rates in this filing may need to change materially to ensure adequacy with expected market costs.

...Reasons for Proposed Rate Change

The following components are significant factors contributing to the proposed rate change: medical trend and utilization, financial experience, and increasing market morbidity.

...4.4.3.2(a): Morbidity Adjustment

This assumption reflects the anticipated change in morbidity from calendar year 2025 (“base period”) to calendar year 2027 (“projection period”) for BridgeSpan Individual ACA plans. The morbidity adjustment reflects a change in the expected health risk of the pool regardless of the underlying demographics.

...4.4.3.2(b): Demographic Shift

A demographic adjustment is reflected to account for population demographic differences between the experience period and the projection period. Adjustments are developed consistent with current filed factors for age and area.

...4.4.3.2(c): Plan Design Changes

Company experience period claim costs are adjusted to reflect anticipated changes in covered benefits (Essential Health Benefits, Mandated Benefits, and Other Benefits) and changes in cost sharing.

Kaiser Foundation Health Plan of the Northwest:

The fifteen plans covered by this rate filing are renewing benefit plans from 2026. All rate changes for the plans renewing in 2027 are primarily driven by the claims experience of the single risk pool, medical inflation, Risk Adjustment transfer payments, mandated changes to certain plans, taxes and fees imposed on the issuer and changes in APTC driven by the expiration of additional subsidies through the American Rescue Plan Act (ARPA) and reduced APTC due to the continued rollout of the BHP. The proposed average rate change can be seen on Exhibit 1. The average rate change does not indicate that every member’s rate will change by this amount, as rates are affected by the ages of those covered, county of residence and benefits chosen.

...The morbidity adjustment (see Exhibit AM5) reflects the change in the expected health risk from the 2025 experience period to the 2027 projected single risk pool, independent of underlying demographic changes. The adjustment to morbidity has been developed to reflect the material impact of fixed costs as a result of KFHP’s integrated delivery model.

In this filing, ARPA premium subsidy is projected to be discontinued in 2026, and projected membership is then projected to have higher morbidity than the base. Thus, the morbidity adjustment is modified to reflect the deterioration in the projected population’s morbidity.

Moda Health Plan, Inc:

he average rate change is 25.0%. The proposed rate increase varies by product and plan and rates in the filing vary by plan, age, and geographic area. The average rate change was calculated by comparing the weighted average premium for current members on the existing plans and rates to the weighted average premium for members on the 2026 plans and rates.

The proposed rates and analysis included in this filing are based on state and federal laws and policies in place at the time of submission. Any subsequent changes will impact the appropriateness and adequacy of the proposed rates.

The adjustments included in the proposed rate change include adjustments for the shift in metallic tiers, cost and utilization trends, changes in taxes and fees, the Oregon Reinsurance Program, as well as CSR loading to silver plans.

...Morbidity Adjustment: A 1.040 adjustment was made to reflect the change in expected risk of the pool between the base period and the projection period. The change in population and enrollment driven by the expiration of the enhanced premium tax credits is the main driver of the morbidity adjustment. This has been observed with market enrollment decreasing in 2026 and a shift in emerging 2026 utilization trends.

In other words, 4 points of the 25% overall requested increase is due to the continuing impact of the enhanced subsidies expiring back in December.

Regence BlueCross BlueShield of OR:

This filing proposes an average annual rate change of 12.2% at January 1, 2027, for the Individual line of business, as shown in “Exhibit 1: Development of Rate Change”. The 2027 projected average premium is $814.53 per member per month (PMPM).

The average annual rate change is calculated based on Individual enrollment data as of March 2026 and includes the mapped rate impact for membership enrolled in plans terminating in 2027. A summary of the rate changes by plan is shown in “Exhibit D1: 2027 Average Change in Plan Base Rates”.

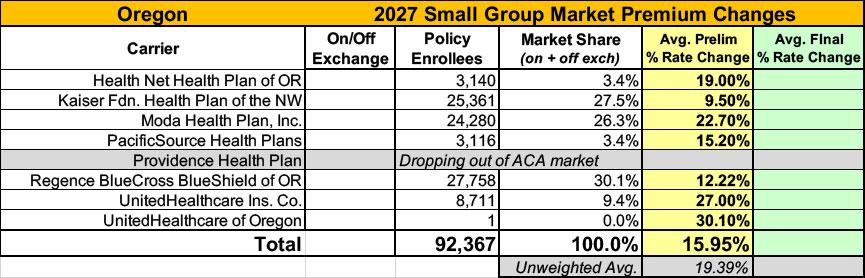

Overall, the four carriers are asking for weighted average increases of 17.2% for the individual market and 16.0% for the small group market in 2027.

| Attachment | Size |

|---|---|

| 409.86 KB |

Advertisement